Brisk weather and the upcoming holidays may signal the end of 2022, but many opportunities still exist to capture immediate and future savings for manufacturers and distributors. Use the same energy and drive that was present throughout the year to take swift, decisive action now to identify and implement tax savings that can impact your bottom line.

Brisk weather and the upcoming holidays may signal the end of 2022, but many opportunities still exist to capture immediate and future savings for manufacturers and distributors. Use the same energy and drive that was present throughout the year to take swift, decisive action now to identify and implement tax savings that can impact your bottom line.

Work Opportunity Tax Credit

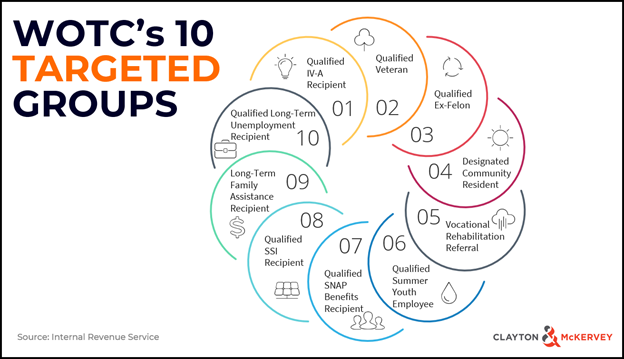

Employers who bolster their workforce by hiring and employing individuals within 10 targeted groups can benefit from federal tax credits this year with the Work Opportunity Tax Credit (WOTC). All sizes of organizations are eligible to claim the WOTC with there being different filing methods for taxable and tax-exempt employers.

The Consolidated Appropriations Act, 2021 authorized the extension of the WOTC until December 31, 2025, to encourage access to good jobs for those who face significant barriers to employment.

The WOTC is equal to 40% of up to $6,000 of wages ($2,400) for employees that are certified as being within one of the 10 target groups, are in their first year of employment with the company and have performed at least 400 hours of service for the employer. Prorated amounts can be earned for at least 120 hours of work. Rehired workers are excluded from the program. Generally, unused WOTC can be carried back one year and forward 20 years.

- Evaluate whether using a carryforward you had from 2021 would be beneficial for you to claim this year

- Have HR review your 2022 first-year employees and determine which people qualify for providing you with a tax credit

- If open positions exist, encourage focusing recruiting efforts on jobseekers within one of the 10 targeted groups.

- Ask employees to refer individuals with the skill sets and aptitude you need

State and Local Tax Considerations

Despite hopes getting high when the Inflation Reduction Act of 2022 (IRA) was being negotiated, the federal state and local tax (SALT) burden for pass-through entity (PTE) business owners remains in place. However, the $10,000 limitation of the SALT deduction can be circumvented by pass-through entities (S corps, LLCs, partnerships) in several states, including Michigan, when an election is made to opt into the state’s PTE tax regime.

Performing an annual review of your state “nexus” footprint and related analysis of those states PTE rules can result in significant tax savings.

Nexus and Voluntary Disclosure

Everyone who buys, sells, has offices, plants, warehouses, staff, or consultants in more than one state should be familiar with each state’s nexus requirements and the impact of the supreme court decision in the Wayfair case. Armed with that knowledge, you should review your state activities to determine whether you have triggered nexus in a new state or whether you have triggered nexus in past years.

The court ruling under Wayfair expanded the ability of states to assess taxes on businesses where they not only have a physical presence but also where they have an economic tie. These relationships—nexus—extend to all types of taxes including sales & use, payroll, and income/franchise taxes.

Filing in and allocating all of your income to your home state(s) is not a reasonable position and more than likely will result in exposure to tax liabilities in other states. Should you be contacted by a non-filing state they will usually review all activity and assess tax, penalty and interest for up to eight (8) taxable years. The issue gets expensive when the exposure in other states extends beyond the normal statute of limitations (normally 3 or 4 years) for amending returns in your home state(s) to request refunds for tax paid on income now subject to tax in a new state.

The good news is that most states have Voluntary Disclosure programs where they provide favorable terms to companies that come forward and submit a Voluntary Disclosure Agreement. This may reduce your tax obligation to a limited number of years and waive expensive penalty assessments. Voluntary disclosure agreements should always be considered when assessing your multi-state tax exposures.

Clean Manufacturing Investment

A clear win for the manufacturing sector in the Inflation Reduction Act is the $10 billion dollars appropriated in the form of tax credits to build or expand facilities that produce clean technologies such as solar, battery, wind, electric vehicle and energy efficiencies. A grant program will help industrial facilities reduce their emissions; and in a separate initiative, installations that achieve at least a 20% reduction in greenhouse gas emissions can now include those expenses when applying tax credits.

Finding Your Tax Efficiencies

Manufacturers and distributors are a critical part of the nation’s infrastructure and economy so staying strong and pivoting when needed will always be part of the plan. Products and methods of production shift and adapt, as will the tax laws that govern them.

Continue the Conversation

If you would like assistance with evaluating your tax position to identify available opportunities, contact Clayton & McKervey for a consultation to learn how tapping into our industry research and expert guidance can help make it easier for you to shore up your bottom line.